New York State Insurance Department: A Look Back

(The following article is reprinted with permission from the July 2011 issue of INSide News, the New York Insurance Department’s internal newsletter)

The New York State Insurance Department regulates more than 1,700 business entities with more than $4 trillion in assets. On a stand-alone basis, this represents the seventh largest insurance market in the world.

The world and the insurance industry have changed dramatically since the Insurance Department was founded in 1860, but the Department's core mission of protecting policyholders and fostering the development of a sound, vibrant insurance industry remain unchanged.

The Department will soon open a new chapter in its history as it merges with Banking into the new Department of Financial Services, but here's a look at the last 150 years of insurance regulation in New York.

|

|

|

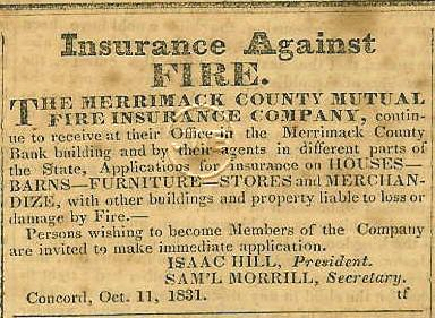

Insurance emerged in the United States in the 18th and 19th Centuries, principally as a form of protecting property owners from fire losses on land and marine losses at sea. The first American insurance company was founded in 1735 in South Carolina.

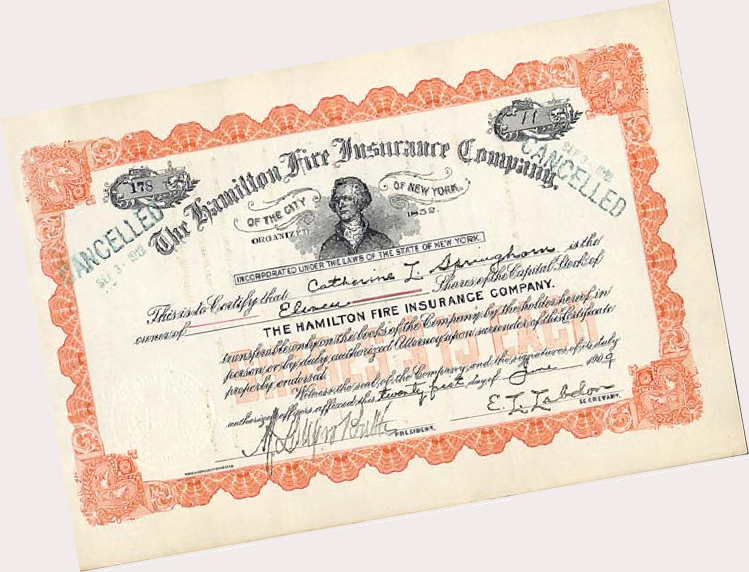

Through the first part of the 1800s, the business of insurance was commonly conducted under special incorporation charters granted by state legislatures. In New York, some 140 insurance companies were incorporated by special act. Domestic insurance companies in New York were first required to file sworn annual statements by legislation passed in 1829. The legislation authorized the Comptroller’s office to be the depository of these statements. |

Need for Greater Oversight

The need for more focused oversight of the insurance industry became evident as New York grew as a commercial and transportation center. All but three of New York City’s 26 fire insurance companies went bankrupt after the Great Fire of 1835 destroyed nearly 700 buildings in the city’s business district in Lower Manhattan.

New York’s Constitution of 1846 ended the cumbersome process of granting special charters to incorporate insurers. The new Constitution required the companies to be organized under general state laws. In 1849, the Legislature approved legislation requiring the Comptroller to administer existing laws covering marine, fire and other early forms of insurance. Two years later, the Comptroller was given the discretionary power to appoint individuals to examine life insurance companies, although there were no provisions for regular examinations.

‘Government Meddling’

The first attempts to create a separate insurance department were made in the 1850s as it became apparent that even periodic examinations of insurers by the Comptroller’s office were found to be inadequate. Insurance companies opposed these initiatives as “paternalism” and “government meddling.”

Legislation creating an insurance department independent from any other office or department in the state was approved in 1859. The legislation called for the appointment of a single, full-time superintendent and authorized an Insurance Department independent from any other state office or department. The cost of supporting the new department – on a recommendation from the insurance industry – was to be borne entirely by industry assessments.

First Superintendent

When the legislation became effective on Jan. 1, 1860, William F. Barnes took office as the first Superintendent of Insurance. An accountant, attorney and politician who became interested in insurance as a member of the Comptroller’s office, Barnes supervised the filings of 155 fire insurance companies and 16 life insurance companies during his first year in office.

Examinations became the cornerstone of supervision during the two-year term of the second Superintendent, George W. Miller, who took office in 1870. Statement audits filed by insurers were supplemented by periodic visits to company offices to verify the accuracy of the statements insurers submitted.

By the 1870s, each state had some form of insurance regulation and most had an insurance department or agency. However, differing state requirements for annual statement forms and other submissions led to confusion in the industry. The industry’s growth was also stunted because states required separate deposits from insurers seeking to conduct business in their jurisdictions. As a result, small companies with limited assets were effectively discouraged from growing.

More Uniform Supervision

In 1871, Miller invited insurance commissions from the other states to meet in New York to strive for a more uniform approach to industry supervision. “As the people of every state are interested in procuring insurance which shall be reliable, and at the same time, cost as little as possible, it would seem that some measures…ought to be adopted which would tend to promote the general interests of the insurer and the insured,” he said.

Eighteen states met later that year for the first session of the National Insurance Convention and elected Miller as the group’s first president. The group sponsored the Reciprocal General Insurance Act of 1871 to promote uniform law, regulations and supervisory practices. “The true object and aim of governmental supervision should be to afford the fullest possible protection to the public, with the least possible annoyance or expense to, or interference with, the companies,” Miller said.

The group became known as the National Convention of Insurance Commissioners the next year and its members – now representing 30 states -- urged cooperation across state lines on common insurance issues.

Economic Capital

In the post-Civil War years, New York City emerged as the nation’s economic capital, further encouraging insurance industry growth and innovation. For example, in the 1870s, industrial life insurance for low income workers was marketed door-to-door and gained popular acceptance among thousands of new immigrants who worked in New York’s factories.

The Insurance Law of 1892 codified many provisions which have been passed down to today’s Insurance Law, establishing the first comprehensive compilation of previously existing provisions relating to insurance. These included regulations relating to investment capital and surplus; restrictions of insurers on the purchase or holding of real estate; jurisdiction of the Superintendent over assets, books and accounts of foreign insurers; restrictions on alien insurers; and the authority of the Superintendent over impaired insurers.

As one century closed and another opened, new forms of insurance began to be seen. In 1898, the Travelers Insurance Company issued the first automobile insurance policy. Dr. Truman Martin, of Buffalo, paid $11.25 for the policy, which gave him $5,000 in liability coverage. It’s not known if Dr. Martin ever had to file a claim. In 1910, New York became the first state to issue workers’ compensation insurance, considered to be a major advance in social justice. The insurance was intended to provide financial help to workers injured on the job until they were healthy enough to return to work.

Armstrong Investigation

Mismanagement in the life insurance business that included exorbitant salaries, questionable investments and excessive commissions resulted in a 1905 investigation into insurance company practices. The investigation, known as the Armstrong Investigation, was conducted by Charles Evans Hughes, a 43-year-old attorney who would later become the state’s 36th Governor, a presidential candidate and Chief Justice of the U.S. Supreme Court.

The Armstrong Investigation led to the passage of a New York law in 1907 that spelled out a series of reforms and became a model for life insurance legislation adopted in a number of other states. The reforms:

- Required mandatory periodic examinations of all life companies.

- Established Civil Service requirements for examiners, a step which raised the standards of life supervision throughout the country.

- Set reporting requirements for lobbying expenditures and requirements prohibiting some political contributions.

While bringing to light abuses, the Armstrong Investigation also demonstrated that the majority of the life companies were essentially sound. The investigation also helped educate the public on the benefits of life insurance and encouraged a higher sense of trusteeship among the managers of life companies.

Regulatory Oversight

In 1911, legislation was approved requiring the Department to regulate all insurance rates, except those for life, accident and health and marine insurance. The Department was charged with making sure rates were reasonable and adequate and not unfairly discriminatory.

During the Great Depression, the Department promoted new rules clarifying insurer investment requirements, setting more equitable determination of cash surrender values and forfeitures, and recognizing up-to-date values and improvements in mortality tables.

In 1933, Superintendent George S. Van Schaick took decisive action to curtail the drain of cash from life insurers through policy loans and surrenders after the Bank Holiday when banks closed their doors to deposit withdrawals. Van Schaick recognized that excessive payment of cash might force the sale of investments at a time when the securities markets were already strained. He also promoted legislation to modernize the insurance statute covering insurer liquidations by focusing first on conservation and rehabilitation and using liquidation only as a last resort.

The years of the Great Depression also saw the emergence of new and important types of insurance coverage through the Blue Cross and Blue Shield organizations, forerunners of today’s health care insurance programs.

State Insurance Regulation

Robert E. Dineen was appointed Superintendent in 1943 at the height of World War II. It was his challenge to preside over the Department at the time of the South-Eastern Underwriters Association case.

In May 1943, the anti-trust division of the U.S. Department of Justice filed a criminal prosecution in U.S. district court in Georgia against South-Eastern Underwriters, an organization of fire insurance companies, and against its officers and member companies. They were charged with conspiracy to fix and maintain arbitrary and non-competitive rates. The government contended the defendants monopolized trade and commerce in the fire insurance industry in several states.

For more than 75 years, the Supreme Court had held that insurance was not commerce and that insurance companies were not engaged in interstate commerce. South-Eastern Underwriters maintained that the government was asking the court to overturn the attitude of the Court, Congress and the states. The district court and later the Supreme Court ruled that the Sherman Anti-Trust Act did, in fact, apply to the business of insurance and, therefore, could be regulated by Congress.

Recognizing the significance implications of the change, Dineen and other state insurance commissioners worked through the National Association of Insurance Commissioners (NAIC) proposing federal legislation that would keep the business of insurance under state supervision. They also proposed that insurance industry be allowed to engage in reasonable cooperative procedures which were necessary to establish such things as statistical rates bases, rates and coverage.

Later, Congress passed and President Franklin D. Roosevelt signed the McCarran Act, which established that federal anti-trust laws did not apply to the business of insurance as long as the states elected to regulate the industry.

Superintendents of Insurance, 1860 to 2011

No |

Name |

Time Served |

1 |

William Barnes |

Jan. 1860 – Feb. 1870 |

2 |

George W. Miller

George B. Church* |

Feb. 1870 – May 1872

May 1872 – Nov. 1872 |

3 |

Orlow W. Chapman

William Smyth* |

Nov. 1872 – Jan. 1876

Feb. 1876 – Feb. 1877 |

4 |

John F. Smyth |

Feb. 1877 – Apr. 1880 |

5 |

Charles G. Fairman |

Apr. 1880 – Apr. 1883 |

6 |

John A. McCall, Jr. |

Apr. 1883 – Dec. 1885 |

7 |

Robert A. Maxwell |

Jan. 1886 – Feb. 1891 |

8 |

James F. Pierce |

Feb. 1891 – Feb. 1897 |

9 |

Louis F. Payn |

Feb. 1897 – Feb. 1900 |

10 |

Francis Hendricks |

Feb. 1900 – May 1906 |

11 |

Otto Kelsey

Henry D. Appleton* |

May 1906 – Jan. 1909

Jan. 1909 – Feb. 1909 |

12 |

William Hotchkiss |

Feb. 1909 – Feb. 1912 |

13 |

William T. Emmet |

Feb. 1912 – Apr. 1914 |

14 |

Frank Hasbrouck |

Apr. 1914 – June 1915 |

15 |

Jesse S. Phillips

Henry D. Appleton* |

July 1915 – Oct. 1921

Nov. 1921 |

16 |

Francis R. Stoddard, Jr. |

Dec. 1921 – June 1924 |

17 |

James A. Beha |

July 1924 – Dec. 1928 |

18 |

Albert Conway |

Jan. 1929 – June 1930 |

19 |

Thomas F. Behan

Henry A. Thellusson* |

July 1930 – Feb. 1931

Feb. 1931 – Mar. 1931 |

20 |

George S. Van Schaick |

Mar. 1931 – May 1935 |

21 |

Louis H. Pink

Thomas J. Gullen* |

May 1935 – Jan. 1943

Feb. 1943 – Sep. 1943 |

22 |

Robert E. Dineen |

Sep. 1943 – June 1950 |

23 |

Alfred J. Bohlinger

Adelbert G. Straub, Jr.* |

July 1950 – Jan. 1955

Feb. 1955 |

24 |

Leffert Holz |

Feb. 1955 – Mar. 1958 |

25 |

Julius Wikler |

Mar. 1958 – Jan. 1959 |

26 |

Thomas Thacher

Samuel C. Cantor* |

Jan. 1959 – Oct. 1963

Oct. 1963 – Jan. 1964 |

27 |

Henry Root Stern, Jr. |

Jan. 1964 – Dec. 1966 |

28 |

Richard E. Stewart |

Jan. 1967 – Dec. 1970 |

29 |

Benjamin R. Schenck

Lawrence O. Monin* |

Jan. 1971 – Mar. 1975

Mar. 1975 |

30 |

Lawrence W. Keepnews

John Gemma* |

Mar. 1975 – Apr. 1975

Apr. 1975 – June 1975 |

31 |

Thomas A. Harnett

John Lennon* |

June 1975 – July 1977

July 1977 – Jan. 1978 |

32 |

Albert B. Lewis |

Jan. 1978 – Mar. 1983 |

33 |

James P. Corcoran

Wendy E. Cooper* |

Mar. 1983 – Jan. 1990

Jan. 1990 – June 1990 |

34 |

Salvatore R. Curiale |

June 1990 – Dec. 1994 |

35 |

Edward J. Muhl

Gregory V. Serio* |

Jan. 1995 – Dec. 1996

Dec. 1996 – Apr. 1997 |

36 |

Neil D. Levin |

Apr. 1997 – Apr. 2001 |

37 |

Gregory V. Serio |

May. 2001 - Jan. 2005 |

38 |

Howard Mills |

Jan. 2005 - Dec. 2006 |

|

Louis Pietrolungo* |

Jan. 2007 – Feb. 2007 |

39 |

Eric R. Dinallo |

Feb. 2007 – July 2009 |

|

Kermitt Brooks* |

July 2009 – Aug. 2009 |

40 |

James J. Wrynn |

Aug. 2009 - present |

* Deputy Superintendent with title of Acting Superintendent

© 2011 |